{kind=link}

Ever notice how a company's bond rating can feel a bit like getting a report card? It boils down all the complicated financial details into an easy-to-understand score that shows how good a company is at paying back its debt. This way, as an investor, you can quickly tell which bonds feel as secure as a trusted savings account and which ones might carry a bit more risk. By turning these assessments into simple ratings, you can decide where your money might be safest or where it could get you bigger gains. Isn’t it interesting how clear ratings can boost your confidence when you're investing?

Corporate Bond Ratings Shine with Clarity

Corporate bond ratings are like a school report card for companies that issue bonds. They show how well a company can pay back the money it borrows, just like a teacher checks if homework was done right. Agencies such as S&P Global, Moody’s, and Fitch, along with local experts like CRISIL, ICRA, and CARE, look at a company’s cash flow, debt, and market position to come up with a score.

These ratings use a simple scale that starts with AAA and goes down to D, which means the company has defaulted. Bonds with ratings between AAA and BBB– are seen as safer choices, much like keeping money in a steady savings account. On the other hand, bonds in the BB+ range and lower are riskier, similar to investments that might pay off big but come with more ups and downs.

When a company’s financial health or market conditions change, the ratings can go up or down. For instance, if a company’s cash flow drops, an agency might lower its rating, which in turn can change how much it costs for the company to borrow money. This system helps investors decide if a bond fits with their comfort level and financial goals.

Corporate Bond Rating Scales: Interpreting Credit Grade Levels

Rating scales are important because they give everyone the same way to understand how risky a bond might be. They take complicated financial reports and break them down so you can quickly tell which bonds are safer and which ones might give you bigger, but riskier, returns. Did you know that a AAA-rated bond has historically defaulted less than 0.2% of the time? That makes it one of the safest investments out there.

| Rating Category | Description | Risk Level |

|---|---|---|

| AAA | Top quality with very little risk | Lowest |

| AA | Very strong ability to pay debts | Low |

| A | Good quality but a bit sensitive to the economy | Moderate-low |

| BBB | Decent quality that could face tougher economic conditions | Moderate |

| BB | More vulnerable to bad market conditions | Elevated |

| B & below | Riskier bonds that are more likely to default | High |

Past data shows that bonds with ratings like AAA and AA usually have fewer defaults. On the other hand, bonds in the lower groups, especially B and below, tend to default more often. This clear link between a bond's grade and its risk helps you balance your choices between safety and potential returns.

Global Rating Agencies: S&P, Moody’s, and Fitch in Corporate Bond Ratings

Investors around the world get a clearer picture of credit evaluations thanks to these three agencies. They offer solid frameworks that let you compare a company's financial strength across different markets. This makes it simpler to judge the risk of corporate debt.

Standard & Poor’s Debt Evaluation Framework

S&P looks closely at a company’s balance sheets, cash flows, and industry positions to figure out how likely it is to meet its financial obligations. They offer outlooks like Positive, Negative, or Stable to hint at future changes in ratings based on current trends. In short, they mix hard numbers with personal insights to help you balance risk and reward.

Moody’s Risk Assessment Insights

Moody’s stands out by using models that estimate the chance a company might default and by running stress tests on cash-flow coverage. Their Risk Performance Reports show you how a company might cope with different economic challenges. This not only confirms how a company is doing right now but also points out possible weak spots for the future, a real help for anyone trying to carefully manage risk.

Fitch Market Evaluation Process

Fitch uses a factor-based method, giving clear weightings to things like leverage, liquidity (which means how easily an asset can be turned into cash), and risks specific to each sector. They bring together different metrics and market conditions to paint a complete picture of a company’s credit health. This balanced method helps you catch small changes that might affect a bond’s appeal.

By keeping an eye on these three perspectives, you get a fuller look at market trends. With S&P’s detailed outlooks, Moody’s careful risk models, and Fitch’s structured approach, you have a strong base for making smarter financial decisions.

Corporate Bond Rating Methodology: From Financial Analysis to Credit Scores

Agencies follow a simple, step-by-step approach to figure out a company’s credit score. They blend hard numbers with personal insights from talking with management and watching market trends. This process gives a clear picture of how well a company can handle its debt.

First, they gather all the important data. They closely look at financial ratios and cash flow predictions while also considering factors like management quality and trends in the company’s sector. Sometimes, they even chat directly with the company to get more details.

Next, they dive into the financial statements. This means checking out the income statements, balance sheets, and cash flow records to see how healthy the company really is.

Then, they score various risk factors. For example, they assign points to things like how much debt the company has or how easily it can cover interest payments. This helps measure any weak spots.

After that, a group of experts reviews all this data. They balance the hard numbers with their understanding of market conditions and management style. This committee helps ensure the rating reflects both the math and the more subtle aspects of the company’s situation.

Finally, the credit score is shared with everyone. But the work doesn’t stop there. Agencies continue to monitor the company, updating the score as needed when market conditions or the company’s financial health changes.

This method keeps evolving to match new economic trends and regulatory rules, making sure that the ratings stay useful and trustworthy for investors and companies alike.

Assessing Risk and Yield: Key Factors in Corporate Bond Credit Evaluations

When figuring out how likely a company is to miss a debt payment, we look closely at a few key numbers. We check things like how much debt the company has, how much profit it makes, how steady its cash flow is, and what’s happening in its industry. If a business has a lot of debt compared to what it earns, it may have trouble paying interest on its loans. On the other hand, a company with regular cash inflows and low debt is usually seen as a safer bet. This process helps investors understand if a company can keep up with its debt without hurting its financial health.

The company’s credit rating also tells us a lot about the potential return or yield. Companies with higher, investment-grade ratings tend to offer lower yields because they’re considered safer, kind of like keeping money in a secure savings account. Meanwhile, bonds from companies with lower ratings have to offer higher yields to make up for the extra risk. It’s all about balancing safety with potential reward, those looking for steady income often prefer investment-grade bonds, while others who can take a bit more risk might opt for high-yield options for a chance at greater returns.

Market moods and interest rate changes add another twist to these evaluations. When interest rates rise, the gap in yields between safe, investment-grade bonds and riskier high-yield bonds usually gets wider. This is because investors demand extra return when taking on more risk. Also, changes in a company’s future outlook, whether they’re seen as positive, negative, or stable, can be a clue to what may happen with yields. This ongoing mix of factors helps investors fine-tune their portfolios based on both market trends and personal comfort with risk.

Historical Trends and Future Outlook for Corporate Bond Ratings

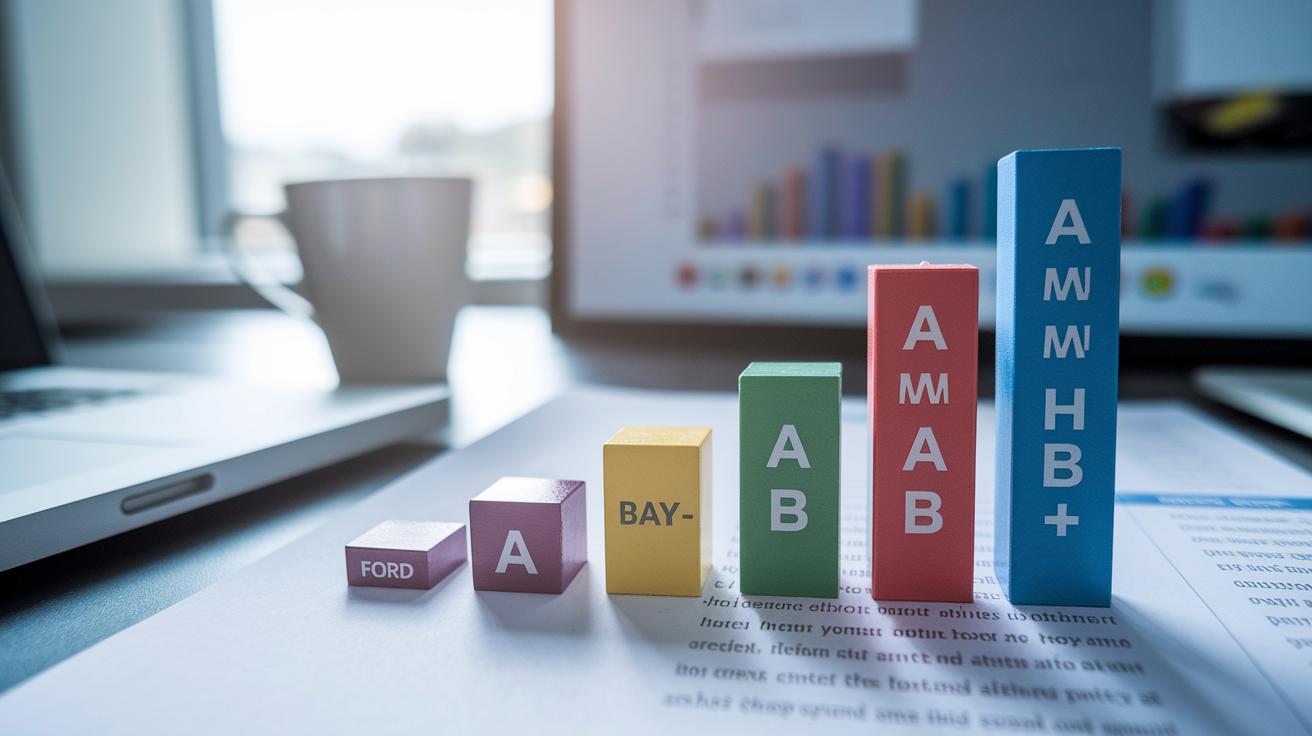

When you look at bond ratings, you can see a clear difference in how likely they are to default. For example, bonds that score top marks like AAA to AA default at only about 0.2% each year, showing just how strong their credit really is. On the other hand, bonds rated BB– and below tend to have default rates near 3.5% annually. This tells us that lower-rated bonds carry a notably higher risk.

Back in 2020, Ford Motor Company went through a big change when its rating slipped from BBB– to BB+. This drop meant many investors who could only hold high-grade bonds had to let go of Ford’s securities. When that happened, Ford’s bond prices fell, and its borrowing costs went up. It’s a good reminder of how one rating change can ripple through the market quickly and force sudden decisions.

Looking ahead, many factors will drive changes in corporate bond ratings. Economic recovery, shifts in monetary policy, and studies of credit in different countries will all play a part. Analysts are closely watching benchmark interest rates and noting that companies in North America often get higher ratings than those in Europe or Asia. In truth, these factors are likely to shape rating shifts and adjustments in yield curves as time goes on.

Final Words

In the action, we explored how credit agencies evaluate a company's creditworthiness and influence borrowing costs through corporate bond ratings. We looked at rating scales and methods used by key agencies to assess risk and yield, all while keeping an eye on historical trends and future outlooks. This quick rundown shows how strategic insights help manage exposure and seize opportunities in today’s market. Stay encouraged and ready to use these insights as you work smartly towards reaching your financial goals.

FAQ

What does a corporate bond ratings chart show?

A corporate bond ratings chart shows the credit quality of bonds, ranking them from top-notch (AAA) to lower ratings. It offers investors a quick guide to understand default risks and issuer strength.

How do bond rating agencies, like S&P, assign ratings?

Bond rating agencies such as S&P evaluate issuer financials and market trends to assign ratings. They provide a snapshot of credit risk, helping investors gauge the likelihood of timely payments.

Where can I look up corporate bond ratings?

Corporate bond ratings can be found on financial websites and directly from rating agencies. These tools help investors track updates, check an issuer’s creditworthiness, and make informed bond purchases.

What is considered a good corporate bond rating?

A good corporate bond rating typically falls within the investment grade range (AAA to BBB–). This rating suggests lower default risk and supports a more conservative, capital-preserving investment approach.

What are the best corporate bond ratings and where can I see a list of AAA bonds?

The best corporate bond ratings, like AAA, indicate top-tier credit quality. Rating agencies and financial platforms often provide lists of AAA-rated bonds, guiding investors toward options with minimal risk.

How do small rating differences like AAA versus AA+ or BBB versus BBB+ work?

Rating increments indicate subtle differences in credit quality. AAA bonds slightly outperform AA+ bonds, while BBB+ bonds offer a bit more strength than BBB bonds, reflecting minor variances in default risk.

What are some examples of bond ratings?

Examples of bond ratings include AAA, AA, A, BBB, and so on. These ratings help investors quickly compare credit risk among bonds and align their portfolios with their risk tolerance.